YOU ARE GETTING READY TO TURN 65 AND START MEDICARE! You may feel overwhelmed, as you will get more mail and phone calls about Medicare and your coverage options. People may even knock on your door.

You may ask yourself, “How do I know which coverage option is the right one for me? What are my choices?”

Let’s start with the basics. Original Medicare Parts A and B are the two parts that come from the Federal Government. This coverage has glaring deficiencies in its coverage. There is no drug coverage, and you will have unlimited liability. This will leave you looking for additional coverage. Now that we know that we have a problem, what is the solution?

There are only two different coverage options for Medicare coverage. You can choose between a Medicare Supplement and a Medicare Advantage Plan.

Choosing the right plan for the right reasons is what we at Sun Coast Legacy Advisors help our clients with.

This magazine is designed to help you answer questions that you might have as you get ready to turn 65. We will first go over the differences between a Medicare Supplement Plan and Medicare Advantage Plan, and then we’ll cover what you should think about when making your decision.

Picking the plan that is right for you will go a long way in making sure you have a smooth transition onto Medicare. We often help clients that picked the plan their spouse had or their neighbor had, but it was not the right plan for them.

Picking the plan that is right for you will go a long way in making sure you have a smooth transition onto Medicare. We often help clients that picked the plan their spouse had or their neighbor had, but it was not the right plan for them.

Turning 65 can be simple and easy. Things to think about are:

• Monthly cost

• Your doctors

• Your prescription drug • Your current health

• Your lifestyle

Sun Coast Legacy Advisors is here to help you through the process. Email or Call to speak to a licensed insurance agent today 888-777-5591 to schedule your appointment today.

What Is Medicare?

Medicare is a fee-for-service health care program in which the government pays health care providers directly for services that fall under Parts A and B, also known as

Original Medicare. It is available to seniors, people on social security disability, and the blind. If you are in need of coverage Original Medicare cannot provide, you can purchase a Medicare Supplement Plan, Part D Prescription Drug Plan or a Medicare Advantage Plan.

Medicare is divided into four categories. This allows you to customize your personal coverage when shopping for a comprehensive policy.

- Part A (Hospital Insurance): Covers hospital care, emer- gency services, nursing home care, home health services and hospice.

- Part B (Medical Insurance): Covers medically necessary services and supplies used for diagnosing and treating medical conditions, and preventative services for illness prevention and/or early detection. Examples include ambulance services, mental health care, outpatient procedures and clinical research.

- Part C (Medicare Advantage): Combines Parts A and B and often part D as well (offered by private companies approved by Medicare).

- Part D: Stand alone prescription drug coverage (offered by private companies approved by Medicare).

LATE ENROLLMENT PENALTIES and INCOME-RELATED MONTHLY ADJUSTED AMOUNT (IRMAA)

Did you know you can be penalized for failure to enroll? If you do not enroll in Medicare Part B when you are first eligible,

your monthly premium may go up 10% for each 12 month period you could have had Part B, but did not sign up – unless you have had creditable coverage during this period.

The Part D late enrollment penalty is an amount that is permanently added to your Medicare drug coverage premium. The cost of the late enrollment penalty depends on how long you went without Part D or creditable prescription drug coverage. Medicare calculates the penalty by multiplying 1% of the national base beneficiary premium by the number of months that you were without coverage.

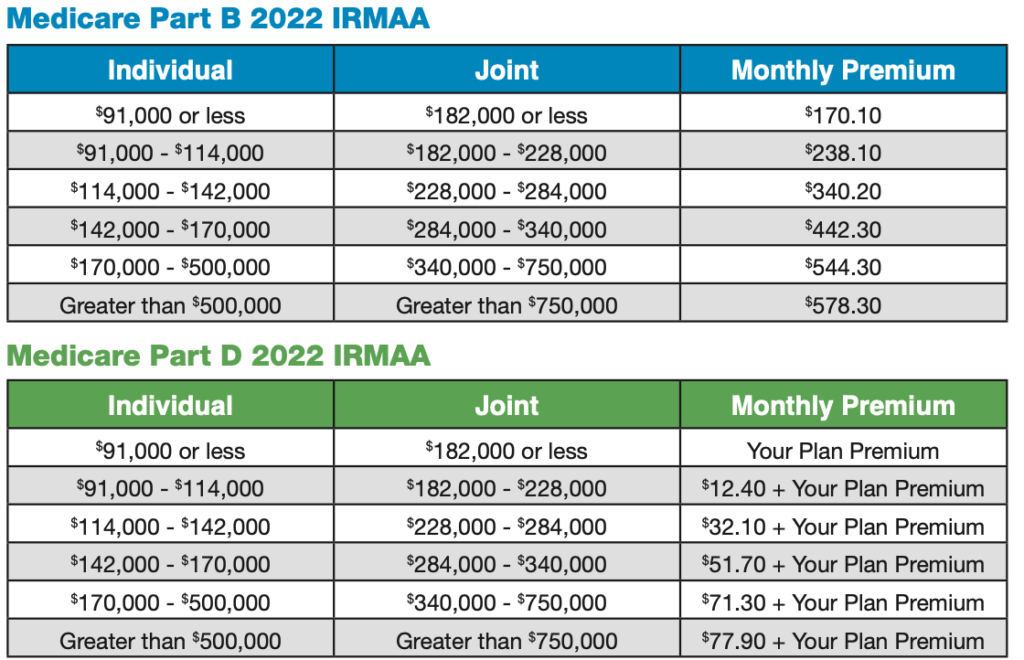

For high-income Medicare beneficiaries, Part B and Part D premiums include an additional

charge based on your modified adjusted gross income. Yes, that is right – Medicare can cost more if your income is above $91,000 a year. IRMAA is determined by income from your prior two years’ income tax returns. This means, that for your 2022 Medicare premiums, your 2020 income tax return is used. This amount is to be recalculated annually.

You will receive a notice from the Social Security Administration to inform you if you have been assessed IRMAA. You can appeal the IRMAA adjustment if you have had a change of life event such as loss of income or divorce.

Receiving a late enrollment penalty or being charged IRMAA does not have to be a surprise. Give us a call today to discuss your Medicare coverage options and what they may cost.

TURNING 65 TIMELINE

The mail and advertisements start coming soon after you turn 64. At this point, it is really too early to start to pay attention to any of the material.

Let’s start out with, “When does your Medicare start?” Your Medicare coverage will start the first day of the month you turn 65. Medicare only has 12 enrollment dates a year, making things really simple. If you happen to be born on the first day of the month, your Medicare coverage will start the month before you were born or age 64 and 11 months.

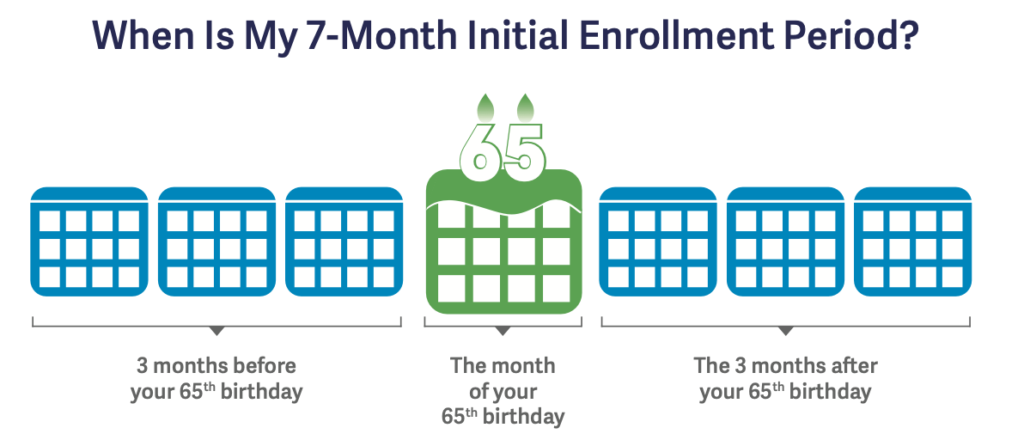

So, now that we know when our Medicare coverage is set to begin, let’s talk about your enrollment period.

This is a seven-month-long window when you can enroll in Medicare Supplements, Medicare Part D stand-alone prescription drug plans and Medicare Advantage plans. This window opens three months before your coverage is set to start. So if you turn 65 in December, your enrollment window begins September 1. Your enrollment window also includes your birth month and three additional months, making the enrollment window seven months long.

Your coverage starts the first day of the month you are born.

If you are getting ready to turn 65, you should start to look into your coverage options about four to five months away from turning 65. One of our agents would be glad to schedule an appointment with you so you can understand what Medicare is going to look like for you and which plan will best suit your needs and wants. Meeting with one of our agents is FREE. The only thing it will cost you is your time. We make all our recommendations based off your needs and wants, so you get the coverage that is best for you. We will continue to maintain this relationship from year to year. As you change and the plans change, we can adjust your coverage annually to make sure your needs are still being met.

DO I NEED TO ENROLL IN MEDICARE?

Whether you need to enroll in Medicare or not is one of the top questions we

get asked about as agents. I have been working with people turning 65 and going on to Medicare for the first time since 2008. People ask us agents most often about enrollment: how to enroll, and what it entails.

Medicare has two main parts called original Medicare or Parts A and B. They are funded by

two different methods. One is voluntary and one is an earned benefit.

Medicare Part A is an earned benefit to those of us in the United States that have worked and paid

our FICA tax for 40 quarters. Once you have your 40 quarters, Medicare Part A is a benefit to you.

You do not have to enroll or sign up for a benefit. When you turn 65, Medicare Part A will be given to you. There is no one you have to call. You do not need to sign up for Part A; simple and easy as that. When you turn 65 and have paid 40 quarters of FICA tax, Medicare Part A is yours.

Medicare Part B is voluntary. You are either conditionally enrolled or you will need to sign up. Medicare Part B is paid through a monthly premium, which in 2022 is $170.10 per month. This can either be billed to you by Social Security if you are not collecting your monthly Social Security Benefit or if you are collecting your Social Security Benefit, they will conditionally enroll you in Medicare Part B and deduct $170.10 a month from your Social Security check.

So this leaves us two groups of people that are turning 65. Those collecting their monthly benefit and those that are not.

If you are collecting your monthly Social Security Benefit then you will be conditionally enrolled and your Medicare card will automatically show up at your address on file with Social Security. You have to do nothing. The card will arrive three and half months before your Medicare is set to begin. So let’s use the example from above. If you’re turning 65 in December, your coverage will begin on December first. Your enrollment period will begin on September first. Which means your Medicare card should arrive in the mail around August 15th. At this point most people are up to their eyeballs in Medicare advertisements coming in the mail. More people than not end up throwing their Medicare card away because it does look like junk mail. Your Medicare card comes from Health and Human services not Social Security or Medicare.

If you are not collecting your monthly Social Security Benefit, you will need to enroll in Medicare Part B. Yes, this means you have to do something to make it happen. You can enroll online at medicare.gov or SSA.gov. You can also to you call Social Security at 1-(800)-772-1213 or go into your local Social Security office. Signing up online by far is the fastest and easiest. You can not enroll in Medicare Part B until your enrollment period begins. Again, this is three months before your coverage is set to begin. If you do nothing, your Medicare Part A only card will arrive about two up after you turn 65.

Enrolling in Medicare is all dependent on whether if you are not collecting your monthly Social or not you are collecting your Social Security Security Benefit.

Original Medicare Overview – Provided By The Government

Not affiliated with or endorsed by any State or the U.S. Government or the Federal Medicare/Medicaid Program.

Medicare Coverage Additional Options- Two Ways To Get Additional Coverage

Not affiliated with or endorsed by any State or the U.S. Government or the Federal Medicare/Medicaid Program.

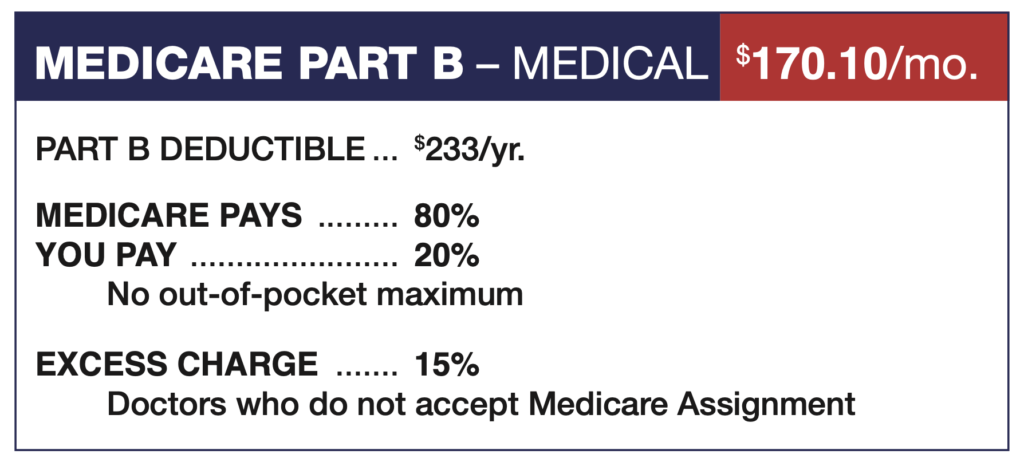

Medicare Part B – Premium Reduction

Medicare Part B has a monthly premium that is charged by the federal government; in 2022 the Medicare Part B premium is $170.10 per month.

Your Medicare Part B premium is either withheld directly from your social security check or Social Security will send you a quarterly invoice for payment.

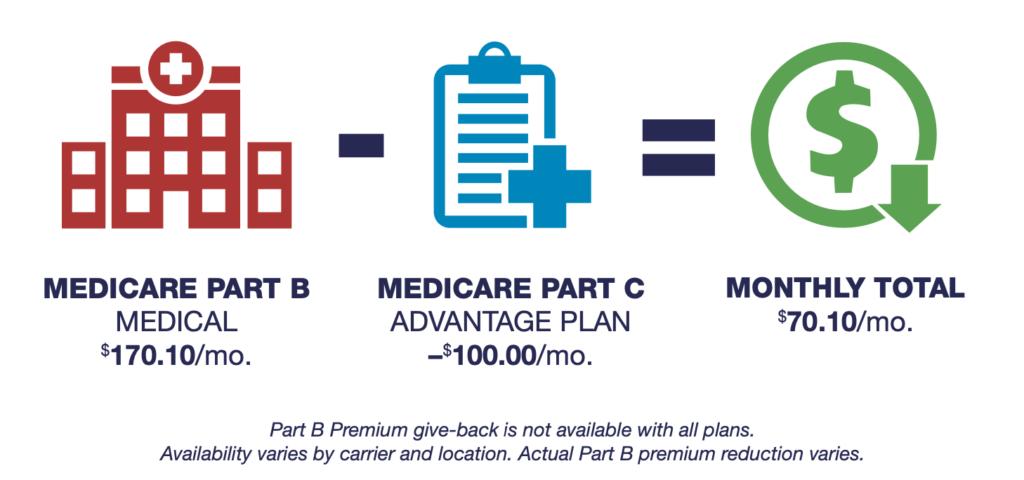

One of your two coverage options for Medicare is to choose to receive care through a Medicare Advantage Plan, also know as Medicare Part C. If you decide to receive care through a Medicare Advantage Plan, Medicare become your secondary insurer, with your Advantage Plan being your primary insurer.

There are many Advantage Plans that now offer a reduction in your Medicare Part B premium as part of the benefits that they provide. So yes, it is possible for Medicare to cost you less than the standard rate of $170.10 per month.

Oftentimes, Medicare Advantage Plans offer Part B reduction of between $70 to $148 per month, reducing your Medicare monthly cost by half to two-thirds of the standard rate charged by the federal government.

Is this right for you? That is the question. Every- one is always looking for the same thing in their insurance coverage. We all want the best insur- ance for the least amount of money.

Things to think about before enrolling in a Medicare Part B reduction Medicare Advantage Plan.

• Does the plan include my doctors?

• What is the Out-of-Pocket Maximum of theplan?

• What are my prescription co-pays on theplan?

• What type of plan is it – HMO vs. PPO?

• What are the co-pays for doctors and hospitals?

Let one of our agents see if a Medicare Advantage Plan with a Part B reduction is right for you. We can show you how this plan may differ from the plan that you are currently enrolled in.

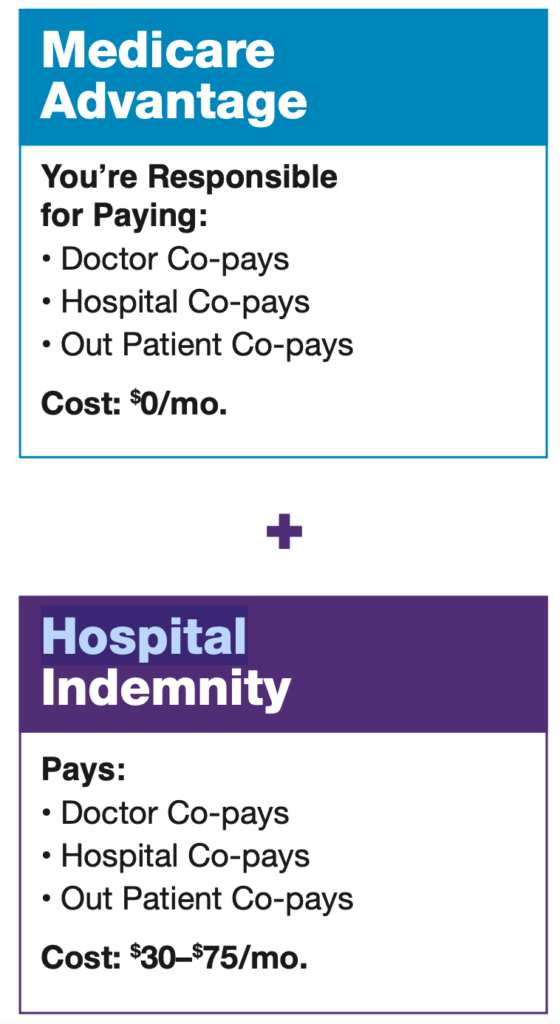

Hospital Indemnity Part B – Flex Insurance Plans

A Hospital Indemnity Insurance Plan can help lower your cost if you have a hospital stay or other qualifying event. While your Medicare Supplement or Advantage Plan may cover some of the cost, they will not cover the entire cost.

Indemnity means protection or security against damage or loss. Hospital Indemnity is designed to do just that — to help protect your savings and your security for the future. Benefits are paid directly to you and in addition to any other health care coverage you may have.

The benefits and premiums for the plans will vary based on the plan options you select. Hospital indemnity plans can help cover hospital admission, doctor office visits, outpatient surgical procedures, ER visits, ambulance services, skilled nursing facility, outpatient rehab and lump sum cancer indemnity.

Adding a Hospital Indemnity to your insurance portfolio can help pay for the unexpected. Call us today to see if adding an Hospital Indemnity plan to your coverage would be right for you. A Hospital Indemnity is not a Medicare Supplement or Medicare Advantage plan.

Not affiliated with or endorsed by any State or the U.S. Government or the Federal Medicare/Medicaid Program.

Hospital Indemnity Part B – Flex Insurance Plans

People often ask us why they would need additional coverage if they are getting Medicare from the government. This is aquestion that we as agents try to answer for the people with whom we help.

Medicare is an insurance program that comes from the federal government. However, there are two major holes in the coverage of Original Medicare (Parts A and B).

Original Medicare does not cover any prescription drugs that you would fill at your local pharmacy. However, if you do not pick up drug coverage when you are first eligible for Medicare Part B, there is a penalty for not having coverage. This forces you to either buy a stand alone Medicare Part D prescription drug plan or enroll in a Medicare Advantage plan that includes Part D prescription drug coverage. If you do not pick up drug coverage and are assessed a penalty, then you will pay a higher premium for the rest of your life. Don’t get stuck with a penalty when you could have picked up coverage for no additional cost if you would have enrolled in one of the many Medicare Advantage plans in the area.

The second hole in Original Medicare is that Medicare leaves people responsible for 20%. Medicare only reduces your risk to 20%. Medicare does not cap your risk. This is the only major type of insurance that I know of that leaves you with open ended risk. Insurance is supposed to cover risk, and Medicare only reduces your risk. Twenty percent of large numbers are large numbers. A hip replacement can cost in the $80,000 range. Twenty percent of $80,000 is $16,000. Don’t be left out in the cold by only having Original Medicare or you could end up owing large medical bills.

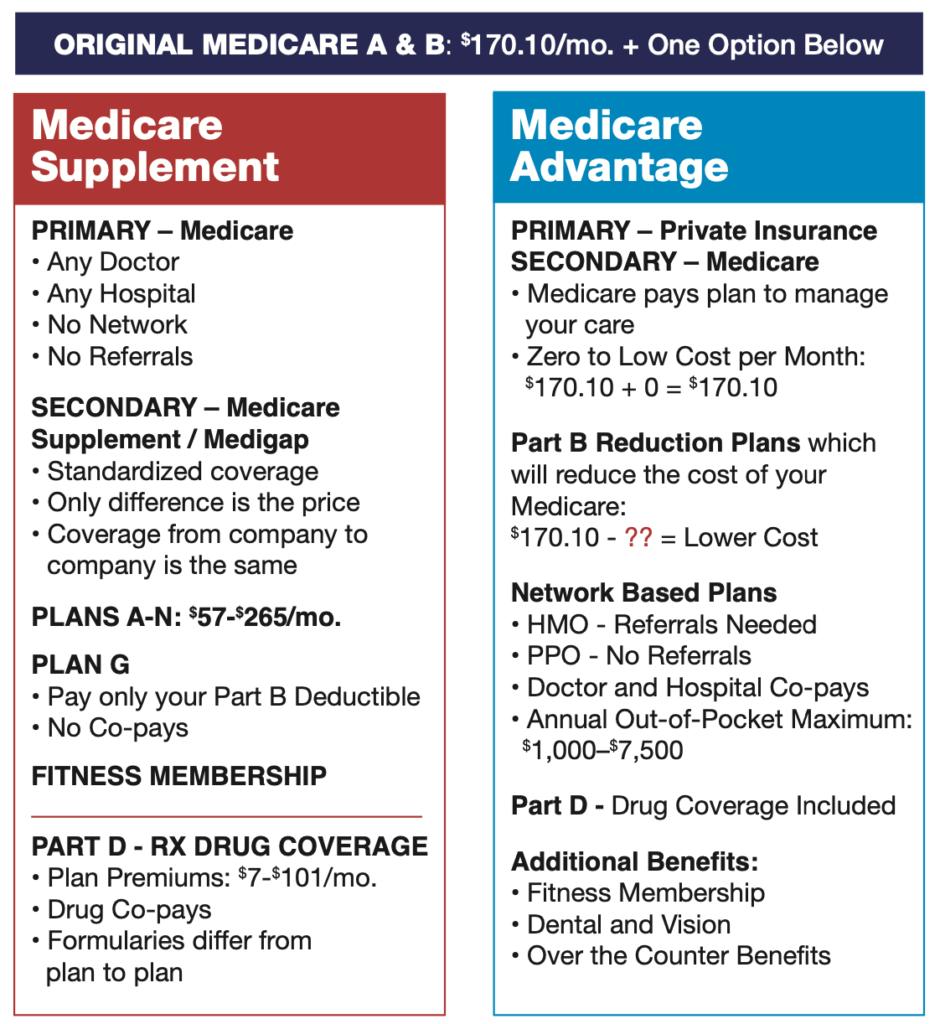

The great thing about Medicare and turning 65 is that you only have two choices for coverage. It may seem like more due to the mail and advertisements that you will receive as you get ready to turn 65. You can either choose to go with a Medicare Supplement Plan, also known as Medigap, or you can choose to go with a Medicare Advantage plan. We will go into why you would choose one plan over another. You must make sure that if you go with a Medicare Supplement that you also choose a Medicare Prescription Drug plan, also known as Part D. If you choose a Medicare Advantage you must make sure that it includes drug coverage because there are some that only cover medical.

Original Medicare is just a starting point. I would recommend that everyone add a supplement or an advantage plan to their coverage so you reduce risk and make sure that you have drug coverage, even if you don’t feel that you need drug coverage at this point.

Medicare Supplement Vs Medicare Advantage Plans

The differences between a Medicare Supplement and a Medicare Advantage plan is often a topic of conversation when approaching the choice between the two. Occasionally, it is not really a choice and after a quick conversation with a broker, you will understand why you will be better off with one or the other depending on your specific circumstances. Here are a few questions to ask yourself before meeting with one of our brokers:

- What will your budget allow your monthly premium to be?

- Does working within a network bother you?

- Do you have doctors you want to keep if your network changes?

- How often do you go to the doctor?

- Do you have any major surgeries on the horizon?

A Medicare Supplement or Medigap policy covers the cost left over by original Medicare. These plans are secondary to Medicare. Medicare is your primary insurer. Having Medicare as your Primary insurer allows you freedom of choice. You can see any doctor that takes Medicare, go to any hospital, no networks and no referrals. Medicare Supplements follow federal and state laws designed to protect you. For that reason, the coverage from company to company providing supplements are the same; the only difference is price. Plan G from one company to the next is exactly the same plan but at a different cost. You will need to add Part D, a stand-alone prescription drug plan. With a Medicare Supplement and Drug plan, you will carry around three different cards: your Medicare card, your supplement card and your Part D card. Your supplement and part D do not have to come from the same company.

A Medicare Advantage Plan, also known as “Part C” or “MAPD Plan.” is an option available where a private company is paid by Medicare to manage your health care. This does not mean you lose Medicare. Medicare becomes your secondary and the private company becomes your primary insurer.

Going with a Medicare Advantage plan does not mean that you are settling for less. There is no degradation in coverage; all Medicare Advantage plans have to cover what Medicare A and B cover. An Advantage plan requires that you have to work within a network. Most often there are HMO and PPO style plans. On an Advantage plan you only incur cost if you incurred care. Meaning, if you go to the doctor or hospital, then you will have a co-payment. The advantage of an Advantage plan is that it provides you with an Out-of-Pocket Maximum. Thus giving you a cap to your liability. Oftentimes, Part D prescription drug coverage is included in these plans. So your doctor, hospital, and drug coverage is all inclusive within one plan.

An Advantage plan requires you to keep your Medicare Part B (Medical) premium current, but has either zero or a low monthly premium. Part B reduction is also available to reduce the cost of Medicare.

The main difference between a Supplement and Advantage Plan is form and function. Supplements have no network where advantage plans do. Supplements have the cost frontloaded in the form of a monthly premium. You are going to pay for coverage every month regardless if you need it or not, but when you do you may pay very little. An Advantage plan has its cost backloaded in the form of a copay. This is a variable cost system where your cost will vary from month to month as you manage your health.

Choosing the right plan depends on your needs and wants. Let us help you in making the right decision.

Still Working And Turning 65?

Iam still working and have insurance coverage through my employer or spouse’s employer. What do I need to do about Medicare when I amgetting ready to turn 65?

This question has a lot of moving parts.

The best thing for us to do is to do a cost benefit analysis as everyone always wants the same thing: the best insurance for the least amount of money.

Let’s start with a few things that are going to determine what you end up doing about your Medicare.

• Cost of your current coverage per month.

Not only do we need to know your monthly cost of the plan, but we would also need to know your annual deductible and out of pocket maximum so that we can calculate your cost and risk.

• Are you insuring a spouse or is a spouse insuring you?

Maybe both you and your spouse are eligible to go onto Medicare. You might be covered under your spouse’s coverage where you are making up the bulk of the monthly cost through the employer. What would their cost be if we removed you from the coverage?

• What is your prescription drug load?

Not only do we want to look at the monthly cost of the plan but we would need to figure in drug cost. On Medicare your drug cost does not go toward your out of pocket maximum. So if you are currently meeting your max out of pocket on your current plan due to drug cost, we might be able to get you a cheaper plan per month, but might end up overpaying for drugs on Medicare compared to your cur- rent plan.

• Size of your current employer?

If you work for an employer of 20 or fewer employees you will want to really make sure we look at this in depth. If you happen to stay on a small employer plan you may be penal- ized for not enrolling in Medicare when you where first eligible.

• Are you collecting your Social Security benefits?

If you are collecting your Social Security, the SSA will conditionally enroll you into Medi- care Part B. What you do not want to do is to stay on your current employer plan and also have Medicare start. You would want to delay Medicare Part B from starting if you are going to stay on your current employer plan.

Again, what it comes down to is that doing a full cost benefit analysis is the best thing to do. To look at all the moving parts we will help you understand the best way to move forward with Medicare.

Give us a call today so we can help you decide if staying on your current coverage or going onto Medicare would be best for you.

History Of Medicare

Medicare was passed into law on July 30th, 1965 at a public ceremony in Indepen- dence, Missouri by President Lyndon B.

Johnson. President Harry S. Truman was present- ed with the nations first Medicare Card. Truman was known as the “Daddy of Medicare.” Medicare services started one year later in July of 1966, covering more than 19 million Americans. In 1972, President Nixon extended coverage to the long term disabled. Medicare Advantage, or Medicare Part C was started in 1997 bringing private insur- ance plans into the market place. Medicare Part D prescription drug coverage was signed into law in 2003 and took effect in 2006. In 2020 there were over 62 million people on Medicare.

HISTORY OF MEDICARE

Here is a timeline of several Medicare and insurance-related milestones:

1945: President Truman calls for a national health insurance program for all. Leg- islators on Capitol Hill don’t act. He asks again in 1947 and 1949. Bills are introduced but die in Congress.

1961: A task force convened by President John F. Kennedy recommends creating a na- tional health insurance program spe- cifically for those over 65. In May 1962, Kennedy gives a televised speech about the need for Medicare.

1964: 1965: President Johnson calls on Congress to create Medicare.

1965: Legislation creating Medicare as well as Medicaid (health care services for certain low-income people and others) passes both houses of Congress by a vote of 70-24 in the Senate and 307-116 in the House. President Johnson signs the Medicare bill into law on July 30 as part of the Social Security Amendments of 1965.

1966: When Medicare services actually begin on July 1, more than 19 million Americans age 65 and older enroll in the program.

1972: President Richard M. Nixon extends Medicare eligibility to individuals under age 65 who have long-term disabilities or end-stage renal disease.

1997: Private insurance plans — originally called Medicare+Choice or Part C, later re- named Medicare Advantage — begin, giving beneficiaries the option of choos- ing an HMO-style Medicare plan instead of the traditional fee-for-service Medi- care program.

2003: On Dec. 8, President George W. Bush greatly expands Medicare by signing the Medicare Modernization Act, which es- tablishes a prescription drug benefit. This optional coverage, for which ben- eficiaries pay an additional premium, is called Medicare Part D.

2006: On Jan. 1, Medicare Part D goes into ef- fect and enrolled beneficiaries begin re- ceiving subsidized prescription drug coverage.